Sometimes the truth isn’t the whole truth.

In the Aug. 25 issue, we considered 12-month returns for S&P 1500 Index stocks since 1994, finding that stocks without dividends averaged returns of 14.3%, a full two percentage points above the average return for divided-payers. In addition, we found that stocks with modest yields (in the 1.0% to 1.8% range) tended to outperform stocks with higher yields, as well as those with very low yields.

That analysis appears solid, simple, and actionable. However, last month a curious reader asked us how much of nonpayers’ outperformance stems from sector trends.

An intriguing question, and worth some exploration.

The premise

Over the last decade, the S&P 1500 Technology Sector Index has delivered a total return of 781%, by far the highest of any sector and far above the 283% of the S&P 1500 Index. Tech stocks are less likely than most to pay a dividend, so the sector has an outsized effect on the average return of nonpayers. In contrast, stocks in the two lowest-returning sectors over the last 10 years, consumer staples and energy, are more likely to pay dividends than the index average, potentially skewing the returns of dividend-payers down.

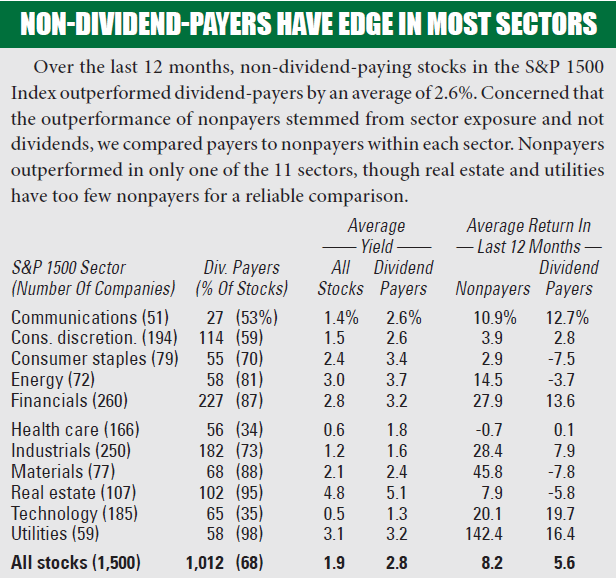

Over the last 12 months, dividend-paying members of the S&P 1500 Index averaged total returns of 5.6%, versus 8.2% for nonpayers, as shown on page 1. Nonpayers outperformed dividend-payers in 10 of the 11 sectors, including all six with yields higher than the index average.

These results suggest nonpayers have an advantage, even in sectors known for dividends. However, one period does not a trend make. We looked at rolling 12-month returns since 1994 for dividend-payers and nonpayers, but compared them within sectors. While every sector of the S&P 1500 contains enough stocks to compute meaningful norms, real estate and utilities tend to have very few nonpayers.

We included utilities and real estate in the table on page 1 because we found the numbers interesting. In the chart at right, we exclude them from our historical analysis. On average, just 5% of real estate companies and utilities have not paid dividends. We distrust signals sent by such small samples.

The results

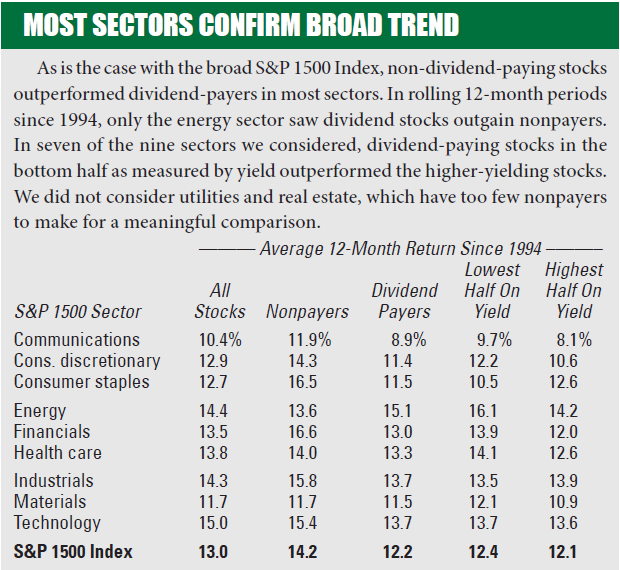

With few exceptions, the trend of nonpayers outperforming dividend-payers has applied within sectors over time. As the nearby table shows, nonpayers’ returns have topped those of dividend-payers in eight of the nine sectors we considered, with energy the only outlier. Nonpayers enjoyed the largest advantage in the financials and consumer-staples sectors, both of which are known for paying solid dividends.

We also took a look at the relationship between higher- and lower-yielding dividend stocks. It turns out that in seven of the nine sectors, stocks in the lower-yielding half of the sector averaged higher 12-month returns than the higher-yielding half. This trend also bears out what we found for the broad index, though the disparity is modest, with the low-yield half outperforming by an average of 0.4%.

Conclusion

This study reinforced our past research that found nonpayers tend to outperform dividend stocks. This conclusion applies in most sectors, regardless of whether stocks in that sector average high or low dividend yields.

We continue to appreciate dividends, particularly those that rise over time. But we also intend to continue fishing in the pool of stocks with no or low dividends, many of which have treated investors well over time.